Payment Aggregator vs Payment Facilitator: What's the Difference?

To stay ahead of the competition in the constantly expanding eCommerce industry, SaaS and software developers require a thorough comprehension of the different types of payment processors available. Two frequently used terms in the payment industry are payment aggregator and payment facilitator. Although they share a connection with payment processing, they are certainly not interchangeable.

It is paramount for SaaS and software businesses planning to accept online payments to understand the dissimilarities between payment aggregators and payment facilitators. Let’s dive into the critical differences between payment aggregators and facilitators as well as their potential impact on your payment processing strategy.

Payment Aggregator

What is a Payment Aggregator?

A payment aggregator is a transaction processing service that helps businesses accept payments without requiring them to create their own merchant accounts. It operates as a mediator between the merchant and the acquiring bank, simplifying the system and allowing merchants to process payments through the aggregator's own merchant account.

This makes it easy and convenient for businesses to begin accepting payments without going through a complicated setup process or enduring ongoing maintenance. Payment aggregators often charge a fee for their services, which can be either a percentage of each transaction or a fixed fee per transaction, depending on the agreement accepted between the two parties involved.

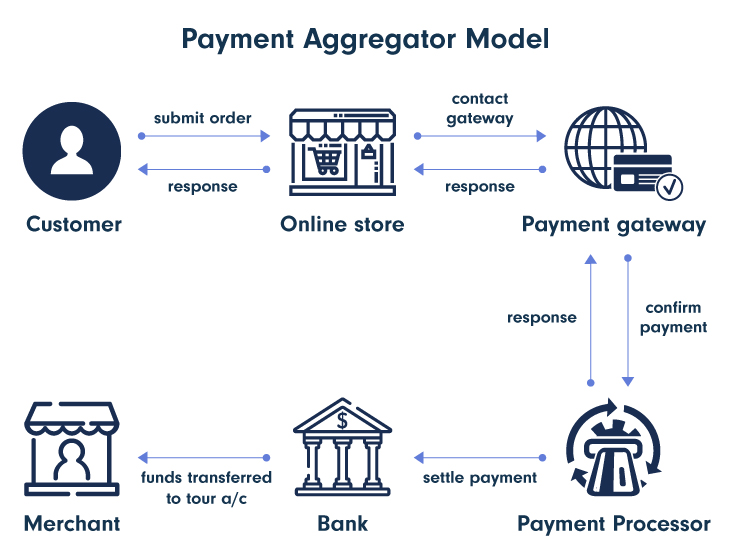

How Does It Work?

This payment solution acts as an intermediary, enabling the processing of payments between a merchant and an acquiring bank.

Here is what happens behind the scenes:

Step 1: The customer initiates a payment transaction on a merchant's website or mobile app.

Step 2: The payment aggregator securely receives the payment information from the merchant's website or app and forwards it to the acquiring bank for processing.

Step 3: The acquiring bank verifies the payment information and approves or declines the transaction accordingly.

Step 4: The aggregator receives the response from the acquiring bank and communicates it back to the merchant's website or app.

Step 5: If the transaction is approved, the payment aggregator deducts its fee and transfers the remaining funds to the merchant's bank account. It is not done immediately, however. The sub-merchants get funded based on a schedule (monthly, weekly, and so on).

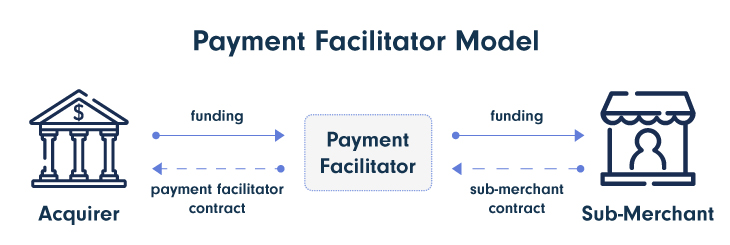

Payment Facilitator

What is a Payment Facilitator??

The payment facilitator model offers merchants a turnkey solution to process transactions, allowing them to set up their own merchant accounts and handle operations on their own.

Additionally, merchants can gain access to value-added services like chargeback management and fraud detection. These payment facilitators can frequently offer editable payment pages, enabling retailers to offer branded checkout experiences to customers.

How Does It Work?

This is how they operate:

Step 1: Retailers register with a payment facilitator and give basic company data, like their legal name, tax identification number, and banking information.

Step 2: To ensure that the merchant satisfies the requirements for processing digital payments, the payment facilitator conducts a risk assessment on them. This could very well mean investigating the merchant's legitimacy, past financial transactions and searching for any red flags pointing to fraudulent conduct.

Step 3: The merchant can begin accepting payments using the platform of the payment facilitator after they have been approved. The facilitator gathers transactions from several merchants and deposits them into a single account.

Step 4: After deducting the monthly fee or other costs, the payment facilitator settles the funds into the merchant's bank account, usually on a daily or weekly basis.

Comparing Payment Services

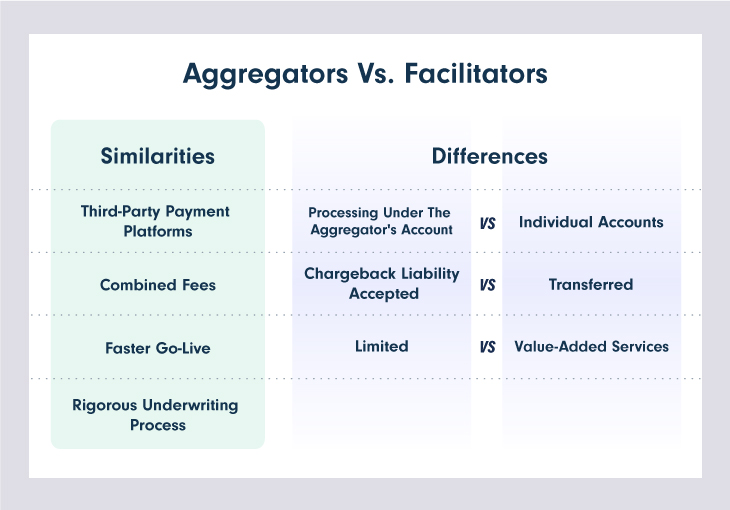

Differences & Similarities Between Aggregators & Facilitators

Payment aggregators and payment facilitators are both types of third-party payment processors. Additionally, both payment options will undergo a rigorous underwriting process, during which each merchant is individually vetted and approved before being allowed to use the payment provider's services.

In terms of processing fees, payment aggregators and facilitators generally charge combined fees, made up of setup, transaction, and monthly fees. However, there may be situations where aggregators could charge a flat transaction fee or a percentage of the transaction amount.

While facilitators offer similar benefits to aggregators, there are also notable differences between the two.

One key difference between payment aggregators and facilitators is the status of merchant accounts. Aggregators typically merge multiple merchants under a single master account, while facilitators create separate accounts for each individual merchant.

Regarding liability for chargebacks, payment aggregators are typically responsible for managing these cases and handling any associated fees or fines, though they will usually pass these fees on to the merchant. However, payment facilitators may pass the full responsibilities and fees on to individual merchants directly.

It is also relevant to mention that payment facilitators will provide merchants with several value-added services like fraud detection and prevention, and detailed reporting and analytics tools.

Despite these differences, payment aggregators and facilitators both offer benefits such as simplified payment processing.

In conclusion, businesses should carefully evaluate their specific needs and priorities in the payment process when deciding between solutions.

Which one is better for your business?

Choosing the right payments partner ultimately comes down to understanding your business's unique needs and priorities. If you're a small business or startup with limited resources, a payment aggregator may be a good option for its simplified processing experience and flat transaction fees. However, if you're a larger business with more complex payment processing needs or a high risk of chargebacks, a facilitator may be a better fit due to its greater flexibility, control, and robust fraud prevention and chargeback management services.

Regardless of your choice, carefully evaluate the features, benefits, and pricing models of each option to determine the best fit for your business. By doing so, you can ensure that your payment processing operations are efficient, cost-effective, and tailored to your specific needs, which will, of course, help you reach your bottom-line profits.

Learn what to consider when choosing a payment solution and its pros and cons on PayPro Global's Blog.

I have worked in digital payment since 2013. I have been a consultant for merchants, an employee for an acquirer and an employee for International Card Scheme. There are so many jargons being used in this space that make many people confused, such as: payment facilitator, payment aggregator, merchant solution provider, independent sales organization (ISO), and so on.

In my simplistic definition, a payment aggregator's job is to aggregate different kind of payments under one umbrella. Meanwhile, a payment facilitator's job is to facilitate the payment process including settlement back from the payer's account to the payee's account. So, let's take an example of Stripe, Stripe job's initially is an easy payment aggregation and, at the same time, they were also a payment facilitator under a global US acquirer (a bank). Now, that Stripe has mature, they can have their own acquiring license. So, Stripe is now a payment aggregator and also an acquirer.

Thank you for your comment!

True, it is so easy to get confused seeing all these payment-related terms. That's why, in our blog, we dive deep into payment trends, payment processing, gateways, MoR, e-commerce, the SaaS industry, and more :)

Really interesting.

I've worked in Mercado Libre (that has Mercado Pago, a payments aggregator) but I didn't know the differences.

Thank you for sharing the knowledge, Marta! I wish you the best, and of course, I'm waiting for more content!

Glad you liked it! Keep an eye on the blog for new insights!