5 signals that made me bet on Godot over Unity

When I started building Ziva in late 2025, the strategic question was not "should I build an AI tool for game developers?" It was "which engine do I bet the product on first?"

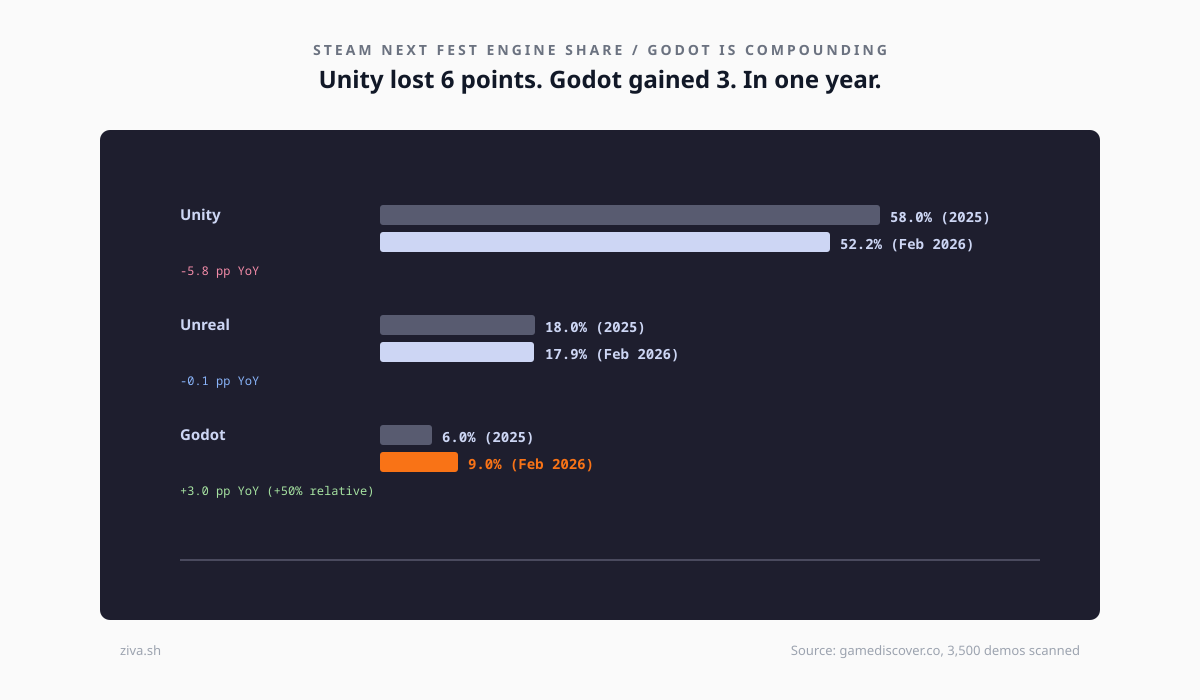

The lazy answer was Unity. It had the largest install base, the most legacy documentation, and roughly 52% of Steam Next Fest demos were built on it as of February 2026. Building for Unity would have been the path of least customer acquisition friction.

I went with Godot instead. Here are the 5 signals that made me pull the trigger, and how each one has held up 4 months later.

1. Godot's Next Fest share grew 50% in a year

Godot accounted for 9% of the 3,500 demos at Steam Next Fest February 2026, up from roughly 6% a year earlier. Unity was at 52%, down from 58%. The directional trend was obvious even if the absolute numbers were still small.

I had seen this pattern before with tooling bets: betting on the incumbent with 52% market share is betting on maintenance. Betting on the one that compounded 50% YoY is betting on the part of the market that is actually moving. Solo and micro-studio devs are the ones picking Godot, and they are also the buyers of my product.

The lesson for other founders: market share at a moment in time is almost useless without the derivative. Two years ago Godot had 4% of this market. Four years ago it had less than 2%. That compounding curve is the signal that matters.

2. The revenue ceiling had been proven

The "Godot is hobbyist only" narrative dissolved in March 2026 when Slay the Spire 2 earned $108M in a single month. That game was built on Godot by Mega Crit, a two-person studio who ditched two years of Unity work after the 2023 Runtime Fee mess.

Before that release, the ceiling for a Godot commercial game was roughly Buckshot Roulette ($6.9M) or Dome Keeper ($6.1M). Those numbers are respectable, but nobody was willing to say "Godot is a serious commercial engine" with a straight face. $108M in 30 days ended that argument.

For a founder building tooling, this matters for exactly one reason: developers pay for tools that help them ship real products. If the ceiling of a Godot game is $6M, the market for serious Godot tools is small. If the ceiling is $100M+, the market becomes "tools that help you take a shot at the real thing."

3. The tooling gap was visible and underserved

When I audited the existing AI plugins for Godot in late 2025, what I found was:

- 3 of the top 5 had been last updated over 12 months ago

- All of them were generic Copilot wrappers without Godot-specific context

- None of them ran the code they generated

- Godot 4 shipped in March 2023, and every AI plugin I tested still hallucinated Godot 3 API names

Compare this to Unity, where Microsoft, GitHub Copilot, Cursor, and at least 4 dedicated Unity AI tools were all actively competing. The Unity market was saturated. The Godot market had a visible gap in "AI tool that actually works for Godot."

Founder lesson: when a market has 2x the addressable demand but 1/10 the tooling competition, that is not bad luck for the big players. That is an entry point.

4. The distribution channels were concentrated

Godot's community is smaller than Unity's, which sounds like a problem until you count the distribution channels.

- Godot's official Discord: 80,000+ active members

- Godot subreddit: 307,000 members

- GodotCon 2025 Munich: 330 attendees

- A handful of Godot YouTubers (GDQuest, HeartBeast, Kaan Alpar) cover basically the entire ecosystem

That last point was the killer. If I could ship a product that was good enough to be shared by 5 Godot YouTubers and 2 Discord admins, I could reach 90% of my addressable market in about 6 weeks. Unity's equivalent reach would require paid ads or a full-time influencer program.

The lesson: "small market" sometimes means "concentrated distribution", which for a bootstrapped founder is better than "large market with fragmented distribution."

5. Godot's technical decisions were actually good

This one was the hardest to evaluate upfront, but the cleanest in retrospect. Godot's scene system is genuinely better architected for an AI agent than Unity's GameObject/Prefab split. Scenes are git-friendly text files, the editor has a live API for reading and modifying the scene tree at runtime, and the whole engine compiles in under 5 minutes from source if I ever need to inspect internals.

Every Unity AI tool I have seen wrestles with two hard problems: the opaque Unity YAML format for scenes, and the lack of a stable editor-running-while-script-runs API. Godot's native architecture removed both problems on day one.

When you build tooling, the underlying software's design choices become your design choices by default. Building on Godot meant I could focus on the AI work instead of spending three months writing YAML parsers.

What happened 4 months later

I do not have headline revenue numbers to share yet. What I can share is what the strategic bet has produced:

- Ziva hit multiple paid customer milestones in its first quarter, with customer acquisition cost under $0 through organic channels (Reddit, Godot Discord, direct recommendations from YouTubers)

- The "Godot YouTuber endorsement" hypothesis held: within 8 weeks, the tool was covered by 3 of the largest Godot educators

- The tooling gap is still there. As of April 2026, I still don't have a direct competitor that integrates at the editor-running-the-game level

Would I make the same bet today? Yes, and more aggressively. The counter-argument ("Unity has 10x the users") is real, but it does not capture that 8 of those 10 users are either AAA studios already served by bespoke tools or casual hobbyists who won't pay for anything.

If you are picking a market for a founder-sized bet, do not optimize for the biggest market. Optimize for the smallest market where the tooling gap is still open and the distribution is concentrated. Everything else follows from that.

Try Ziva if you are building a Godot game. It runs on Godot 4.4 and 4.5, installs in 5 minutes, and gets better every week because we are shipping fast into a market that is still forming.

Betting on Godot's compounding growth over Unity's legacy dominance is a textbook example of picking the right "derivative," ziva.sh. When a two-person studio pulls $100M+ on an engine, the "hobbyist-only" narrative dies, and the vacuum for professional, Godot-specific AI tooling becomes a massive opportunity for a lean founder to own the category.

I’m currently running a project in Tokyo (Tokyo Lore) that highlights high-utility logic and strategic pivots exactly like yours. Since you’ve identified a market where distribution is concentrated and the technical architecture (Godot's scene system) actually supports your AI agent better than the incumbent, entering your project could be the perfect way to showcase this "small market, big gap" strategy while your odds are at their absolute peak.