Merchant Account vs. Payment Gateway: Key Main Differences

If you’re in the process of launching a SaaS product or service, you’ve probably heard of the terms “merchant account” and “payment gateway”. But do you really know what the difference is between the two? And have you worked out which one would be best suited to your SaaS business?

In this article, we tackle the topic of merchant accounts vs. payment gateways so that you don’t have to.

Clearing Up The Confusion

Is a Merchant Account the Same as a Payment Gateway?

No. Simply put, a merchant account allows you to accept credit and debit customer payments. In contrast, a payment gateway forms a connection point between your customer’s bank account and your merchant account.

Is a Payment Service Provider (PSP) the Same as a Payment Gateway?

The short answer is “no.” A PSP creates connections with different payment processors and enhances various transaction types with one solution, facilitating smooth online payments.

When a PSP partners with a new client, the provider sets up a sub-account within one primary merchant account. PSPs are often called “payment aggregators,” as they aggregate the transactions of hundreds of merchants under one account.

On the other hand, a payment gateway is a tool that customers use for completing transaction payments. The gateway processes credit card payments in the front end and handles encryption and verification in the back end.

Merchant Account Basics

What Is a Merchant Account?

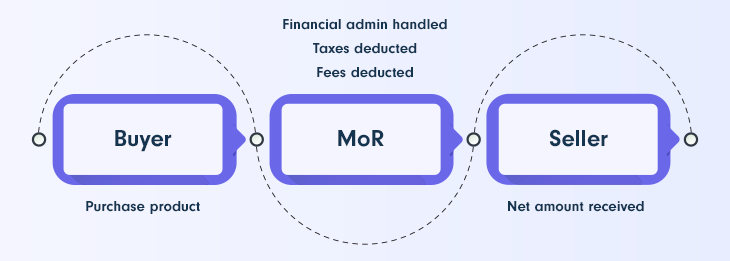

Not to be confused with a Merchant of Record, a merchant account makes it possible to accept credit or debit card payments made via the internet. It’s a specific account set up for this purpose with an acquiring bank or PSP, and your incoming funds are temporarily stored there until the payments are verified.

Your business needs a merchant account if you’re going to process payments through your website using a payment gateway. Money will pass through your merchant account and flow into your bank account.

However, you won’t access funds from the merchant account. It merely acts as a “middleman” between your business and the banks to acquire funds and transfer them into your business account. All the revenue is stored in the merchant account until the settlement date, which typically occurs once a week. Once the funds are settled, they are transferred to your business bank account. Don’t confuse a merchant account with a business bank account!

There are many companies, financial institutions, and banks that provide merchant accounts. Even some payment processors and payment gateways may have merchant services to offer.

Note that a merchant account is accessible to you and anyone authorized to deal with payment information in your business. When you apply for this type of account, you’re given a merchant ID that identifies you as the merchant.

The 2 Types of Merchant Accounts

1. Standard Merchant Accounts vs. Internet Merchant Accounts

An internet merchant account is set up expressly to process online payments with credit or debit cards. A standard merchant account would also be for processing credit card or debit card transactions, but it would be used for card present transactions. This distinction is important because online payments are generally seen as riskier than card-present transactions. As a result, internet merchant accounts often come with higher fees.

2. PSPs and Independent Sales Organizations (ISOs)

PSPs are third-party payment service providers that help merchants process payments. An ISO, in turn, is an independent sales organization that acts as an intermediary between the merchants and the banks that ultimately receive payments. PSP accounts are generally better for smaller- to medium-sized businesses. They are more straightforward, easier to set up, have lower maintenance, and are usually more affordable. ISOs are best for handling larger volumes of sales, although they cost more and they typically have lower transaction fees.

Payment Gateway Basics

What Is a Payment Gateway?

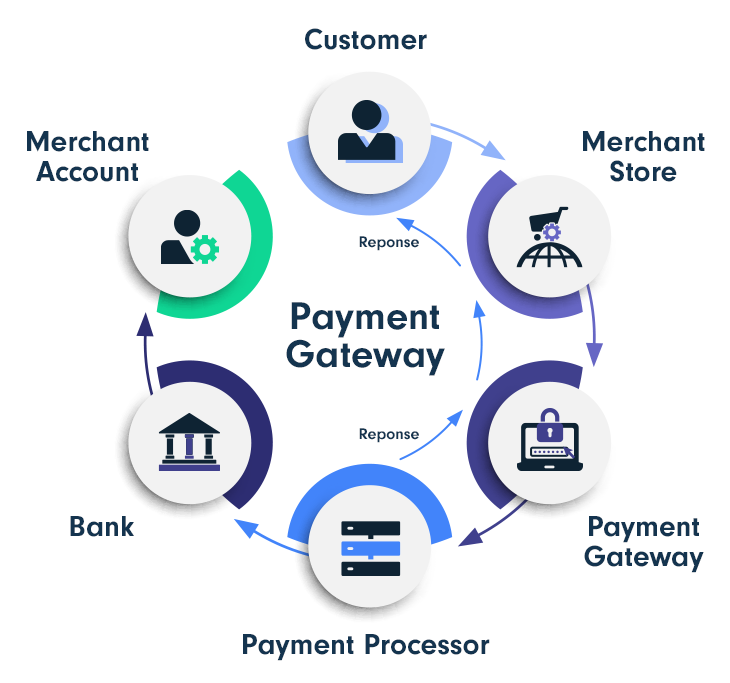

A payment gateway connects your customers’ banks to your merchant account so the funds can go from theirs to yours during payment transactions. The gateway collects all the necessary transaction details and passes them on to your payment processor or merchant account. Thus, customers making online payments don’t interact with your PSP or merchant account — they interact with the payment gateway.

The payment gateway stores and verifies the payment information, ensuring that the money is available, and then transfers the funds to you. This process takes place while making sure the information is entirely secure.

A payment gateway:

- Integrates with your online store.

- Captures details securely from transactions.

- Sends this information to the payment processor or bank.

- Sends a “funds approved” or “declined” message to the merchant.

If the transaction is approved, the customer will be directed to the next step of the payment process.

What Is a Payment Gateway for Credit or Debit Card Processing?

Any business that accepts payments online via credit or debit cards must have a payment gateway. This gateway connects your shopping cart to the next point in the purchase path ‒ which are payment processors, credit card networks, and customers’ issuing banks.

What Is a Payment Gateway Provider?

A payment gateway provider is, quite simply, a business that offers a payment gateway. It is necessary for your business to choose one from a provider to facilitate online transactions on your e-commerce platform. Aside from the obvious, payment gateways are essential for online security during all transaction and fraud screening processes during the entire transaction cycle.

Types of Payment Gateways: Classic Gateways vs. Modern Gateways

A classic gateway requires a more complex process when setting up your merchant and business bank account. A modern gateway, in turn, is all-inclusive and relatively quick to set up. They have shifted their business model to a PSP.

Nowadays, the majority of PSPs and acquiring banks incorporate a gateway service. Plain gateways that only provide this solution are now being deprecated.

Modern gateways are connected to multiple acquiring banks and payment processors, providing the merchant with various merchant account options.

If you’re a larger business transacting worldwide, a modern gateway is probably the better option. This gateway is better suited to large companies because it supports rapid global scaling, offers local payment methods and currencies, and better customer experiences.

Learn the features of payment gateway and merchant account, how it works and how to get one on PayPro Global’s Blog.

The Ultimate Difference Between a Merchant Account and a Payment Gateway

The main difference is best described by the following two scenarios:

A merchant account is a holding bank account that allows your business to accept multiple forms of payment. Payments land here before being moved into your business account. Although you cannot access the merchant account, it’s an intermediary or liaison between your business and the card-issuing banks.

A payment gateway is also a go-between, but this time the interaction is between the customer, their bank account, and your merchant account. The gateway essentially facilitates online transactions and allows your customers to submit payment information securely over the internet.

How Can PayPro Global Help?

As the industry grows, so do the many opportunities for SaaS developers to grow their businesses and enter untapped markets. However, this means facing the complexities of online payments, worldwide compliance, and tax regulations, not to mention the growing threat of online fraud. Having to deal with an increased operational workload, business developers like yourself are left with less time to create new products and improve existing ones. This will inevitably put growth at a standstill.

PayPro Global is the solution you seek. Part of the industry for over 15 years, we offer SaaS, software vendors, digital goods, and gaming creators a unique MoR business model meant to lift the burden of global payments operations off your shoulders. We are your trustworthy business partner, ready to handle your financial, legal, and administrative work. From payments and recurring billing to managing customer disputes, taxes, and compliance, PayPro Global has the tools, infrastructure, and expertise to drive global business growth.