Payment Aggregator vs Payment Facilitator: What's the Difference?

by Marta PoprotskaTo stay ahead of the competition in the constantly expanding eCommerce industry, SaaS and software developers require a thorough comprehension of the different types of payment processors available. Two frequently used terms in the payment industry are payment aggregator and payment facilitator. Although they share a connection with payment processing, they are certainly not interchangeable.

It is paramount for SaaS and software businesses planning to accept online payments to understand the dissimilarities between payment aggregators and payment facilitators. Let’s dive into the critical differences between payment aggregators and facilitators as well as their potential impact on your payment processing strategy.

Payment Aggregator

What is a Payment Aggregator?

A payment aggregator is a transaction processing service that helps businesses accept payments without requiring them to create their own merchant accounts. It operates as a mediator between the merchant and the acquiring bank, simplifying the system and allowing merchants to process payments through the aggregator's own merchant account.

This makes it easy and convenient for businesses to begin accepting payments without going through a complicated setup process or enduring ongoing maintenance. Payment aggregators often charge a fee for their services, which can be either a percentage of each transaction or a fixed fee per transaction, depending on the agreement accepted between the two parties involved.

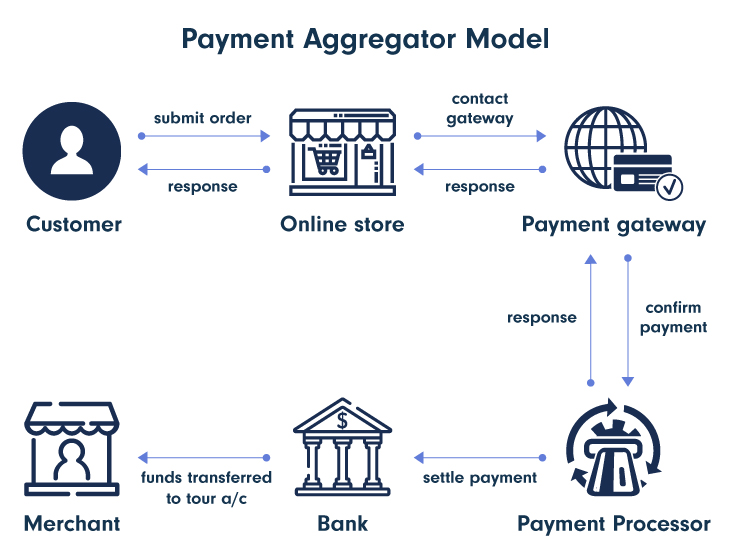

How Does It Work?

This payment solution acts as an intermediary, enabling the processing of payments between a merchant and an acquiring bank.

Here is what happens behind the scenes:

Step 1: The customer initiates a payment transaction on a merchant's website or mobile app.

Step 2: The payment aggregator securely receives the payment information from the merchant's website or app and forwards it to the acquiring bank for processing.

Step 3: The acquiring bank verifies the payment information and approves or declines the transaction accordingly.

Step 4: The aggregator receives the response from the acquiring bank and communicates it back to the merchant's website or app.

Step 5: If the transaction is approved, the payment aggregator deducts its fee and transfers the remaining funds to the merchant's bank account. It is not done immediately, however. The sub-merchants get funded based on a schedule (monthly, weekly, and so on).

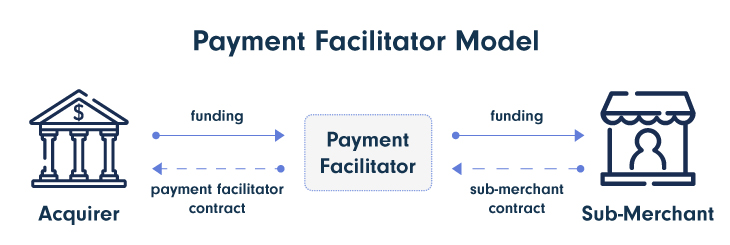

Payment Facilitator

What is a Payment Facilitator??

The payment facilitator model offers merchants a turnkey solution to process transactions, allowing them to set up their own merchant accounts and handle operations on their own.

Additionally, merchants can gain access to value-added services like chargeback management and fraud detection. These payment facilitators can frequently offer editable payment pages, enabling retailers to offer branded checkout experiences to customers.

How Does It Work?

This is how they operate:

Step 1: Retailers register with a payment facilitator and give basic company data, like their legal name, tax identification number, and banking information.

Step 2: To ensure that the merchant satisfies the requirements for processing digital payments, the payment facilitator conducts a risk assessment on them. This could very well mean investigating the merchant's legitimacy, past financial transactions and searching for any red flags pointing to fraudulent conduct.

Step 3: The merchant can begin accepting payments using the platform of the payment facilitator after they have been approved. The facilitator gathers transactions from several merchants and deposits them into a single account.

Step 4: After deducting the monthly fee or other costs, the payment facilitator settles the funds into the merchant's bank account, usually on a daily or weekly basis.

Learn what to consider when choosing a payment solution and its pros and cons on PayPro Global's Blog.